Report: Swiss are richer than ever but wealth inequality persists

The Local - [email protected]

Published: 14 Nov, 2017 CET.

Updated: Tue 14 Nov 2017 11:32 CET

The average household in Switzerland is 35 percent richer than it was at the turn of the century, but there has been no reduction in wealth inequality.

That’s the verdict of Swiss bank Credit Suisse, whose Global Wealth Report 2017, published on Tuesday, named Switzerland as the richest country in the world in terms of wealth per adult for the eighth year in a row.

Switzerland’s wealth per adult figure of $537,600 puts it at the top of the table ahead of Australia and the US in second and third.

For Switzerland, that’s a 130 percent rise since the year 2000, though the report acknowledges that much of that is due to the appreciation of the franc against the US dollar.

In Swiss francs, household wealth rose by 35 percent between 2000 and 2017, an average annual rise of 1.8 percent.

The alpine country also topped the table when it comes to median wealth – perhaps a more accurate reflection of wealth distribution – with a figure of $229,000 per adult.

Swiss adults also have one of the highest debt levels in the world, but this “appears to reflect the country’s high level of financial development rather than excessive borrowing,” said the report.

Unsurprisingly, Switzerland has a proportionately large number of high net worth individuals, with 1.7 percent of the world’s top one percent wealth holders living here, a “remarkable” fact given Switzerland comprises only 0.1 percent of the world’s population, said Credit Suisse.

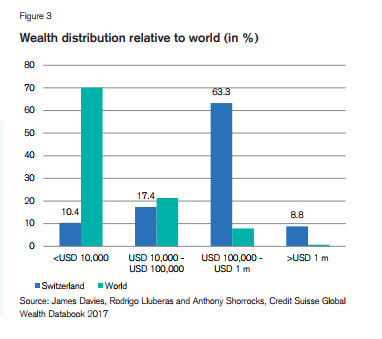

More than 63 percent of Swiss adults have financial assets above $100,000 – compared with under ten percent globally – and nearly nine percent of Swiss residents are US dollar millionaires, far above the global average. An estimated 2,780 people are deemed ultra-high net worth individuals, with wealth exceeding $50 million.

At the other end of the scale, just over ten percent of Swiss adults have less than $10,000 to their name, compared with a whopping 70 percent on a global scale.

Nevertheless, Switzerland has achieved no reduction in wealth inequality since the year 2000, the only country among those with developed economies not to do so, found the report.

Wealth increased significantly across the globe in 2017 to $280 trillion, a rise of 6. 4 percent. Some 2.3 million extra US dollar millionaires were created, including 620,000 in eurozone countries, though the report added that some of this is due to the rise of the euro against the dollar.

The Credit Suisse report comes two months after another report by Allianz said Switzerland had been overtaken by the US in terms of wealth per household, though the insurance company acknowledged that America’s razor-thin lead was in part due to currency fluctuations.

At the other end of the scale, just over ten percent of Swiss adults have less than $10,000 to their name, compared with a whopping 70 percent on a global scale.

Nevertheless, Switzerland has achieved no reduction in wealth inequality since the year 2000, the only country among those with developed economies not to do so, found the report.

Wealth increased significantly across the globe in 2017 to $280 trillion, a rise of 6. 4 percent. Some 2.3 million extra US dollar millionaires were created, including 620,000 in eurozone countries, though the report added that some of this is due to the rise of the euro against the dollar.

The Credit Suisse report comes two months after another report by Allianz said Switzerland had been overtaken by the US in terms of wealth per household, though the insurance company acknowledged that America’s razor-thin lead was in part due to currency fluctuations.

Comments

See Also

That’s the verdict of Swiss bank Credit Suisse, whose Global Wealth Report 2017, published on Tuesday, named Switzerland as the richest country in the world in terms of wealth per adult for the eighth year in a row.

Switzerland’s wealth per adult figure of $537,600 puts it at the top of the table ahead of Australia and the US in second and third.

For Switzerland, that’s a 130 percent rise since the year 2000, though the report acknowledges that much of that is due to the appreciation of the franc against the US dollar.

In Swiss francs, household wealth rose by 35 percent between 2000 and 2017, an average annual rise of 1.8 percent.

The alpine country also topped the table when it comes to median wealth – perhaps a more accurate reflection of wealth distribution – with a figure of $229,000 per adult.

Swiss adults also have one of the highest debt levels in the world, but this “appears to reflect the country’s high level of financial development rather than excessive borrowing,” said the report.

Unsurprisingly, Switzerland has a proportionately large number of high net worth individuals, with 1.7 percent of the world’s top one percent wealth holders living here, a “remarkable” fact given Switzerland comprises only 0.1 percent of the world’s population, said Credit Suisse.

More than 63 percent of Swiss adults have financial assets above $100,000 – compared with under ten percent globally – and nearly nine percent of Swiss residents are US dollar millionaires, far above the global average. An estimated 2,780 people are deemed ultra-high net worth individuals, with wealth exceeding $50 million.

At the other end of the scale, just over ten percent of Swiss adults have less than $10,000 to their name, compared with a whopping 70 percent on a global scale.

Nevertheless, Switzerland has achieved no reduction in wealth inequality since the year 2000, the only country among those with developed economies not to do so, found the report.

Wealth increased significantly across the globe in 2017 to $280 trillion, a rise of 6. 4 percent. Some 2.3 million extra US dollar millionaires were created, including 620,000 in eurozone countries, though the report added that some of this is due to the rise of the euro against the dollar.

The Credit Suisse report comes two months after another report by Allianz said Switzerland had been overtaken by the US in terms of wealth per household, though the insurance company acknowledged that America’s razor-thin lead was in part due to currency fluctuations.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.